In theory, there was no offer. “This is a proposal to judges, not an offer to vultures,” Argentina’s finance minister tweeted at the weekend.

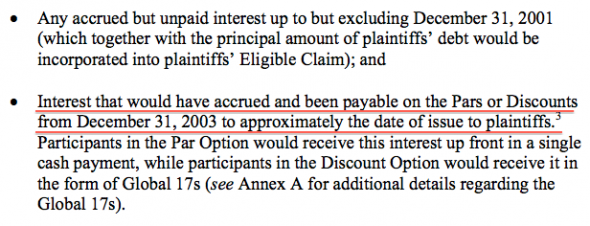

For their part, the three judges of the US Second Circuit had ordered Argentina to tell them “how and when it proposes to make current those debt obligations on the original bonds that have gone unpaid over the last 11 years” (emphasis ours). It’s a last act in the battle that Argentina has been losing to stop restructured debt payments being linked to its defaulted bonds under the pari passu clause.

In practice, the 22-page letter that the government sent to the Second Circuit on Friday — containing “options” for holdouts to take payments “equitably and ratably” with bondholders who swallowed its 2010 debt restructuring, by getting restructuredbonds in place of the original debt — pretty much was an offer.

And — it looks like — not one the judges can accept. Meanwhile, the market haspanicked like wildebeest.

This post is in two parts. The first part covers the similarities of this proposal to the 2010 restructuring, especially where it looks like the Second Circuit would have to be doing considerable “bankruptcy”-type work to approve the proposal as a formula for paying the holdouts. (The court would be cramming down their original contracts, making use of the reality that this is a case about an injunction and a remedy, not a judgement.)

A sovereign bankruptcy regime has long been the holy grail of litigating over government debt. Well, Argentina’s proposal is probably not it.

1) The 2010 debt swap strikes back

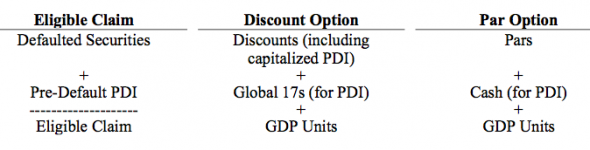

Here’s the basic proposal/offer in a chart (click to enlarge):

“PDI” is post-dated interest, which we’ll come back to briefly. No need to focus on the mechanics of the rest of it that much — it’s a stripped-down version of the 2010 debt restructuring terms. But basically it includes the choice of getting either par bonds that mature in 2038, or 2033 discounts which carry a higher interest rate.

In that case, Argentina has been as good as its political promise not to pay holdouts any better than “the 93 per cent” who wrote down their holdings of its debt in the last decade. And also in that case, the restructured bondholders might be screwed.

This is the kind of “making current” that judges have probably already indicated they don’t think is “equitable” for the terms of the bond contract owned by the holdouts — because it ignores both the acceleration clause in the contract and that NML and others were in their rights to refuse the restructuring offer in the first place.

If the judges go on thinking like this after receipt of Friday’s letter, and then make Argentina pay holdouts upfront and in full — which is the alternative “payment formula” waiting in the judicial wings — then it will default on everyone, or try a risky rerouting of payments.

So, for example, much is already being made of the roughly two-thirds cut to original bond principal that swapping into discounts would involve. It’s a nicely bloody stump for the holdouts to wave in front of the judges, if they’re asked to give their view on Argentina’s proposal.

Then again, the judges only might have signaled this. There’s the other theory that they’re now amenable to a ground-breaking cramdown of holdout claims — shown simply by having sought another formula from Argentina, in language suggesting that the acceleration clause was no longer the be all and end all.

Well, one issue with cramdown… let’s take the following statement from Argentina: “This Proposal is a voluntary option: plaintiffs can choose between being paid “equally” on the same terms as the exchange bondholders, or obtaining, and seeking to execute on, judgments for the full amount of their claim.” Emphasis ours.

That’s a classic “take it or leave it” restructuring offer from a sovereign. Argentina knows perfectly well that “seeking to execute on” judgements against it or any other foreign government — seizing assets — has a snowball’s chance in hell, unless creditors find a creative enforcement strategy. The whole argument against holdouts trying to get relief through the pari passu clause and ratable payment is that this is a veiled enforcement mechanism.

In any case, Argentina’s not seeking to have the judges force the holdouts to give up their claims. But it’s also kind of reminding them why it annoys them so much, and why it’s a bit unseemly to try and make the pari passu case behave like a corporate bankruptcy: lack of enforcement has let Argentina defy US courts until now.

2) The politics of past due interest

“There is a misunderstanding by some that Argentina is not prepared to compensate plaintiffs for past due interest to bring them current,” the Republic notes (rather primly) in its letter. OK, so what about the PDI portion, for making current about 11 years of nonpayment?

So far in this case, NML and the other holdouts have been arguing that Argentina owes them about $1.3bn. When it comes to evaluating that 66 per cent face value haircut, for example… it’s worth noting that this sum mostly reflects post-dated interest. It also includes 9 per cent statutory prejudgement interest levied by the courts, as Argentina seems keen to point out here.

Anyway, the design of the discount bonds seems to load up on PDI, through offering Global 2017 bonds and capitalising the discounts’ principal with amounts of PDI. This is something for the judges to work with, right? Maybe not:

The PDI is calculated on restructured debt, which the holdouts never accepted in the first place, not on their defaulted bonds. It’s quite a sleight of hand, but then this is what the Argentine government is saying: it won’t offer anything better than the debt swaps to date.

Again, it comes back to the judges’ past insistence that the holdouts were in their rights to stay out of those debt swaps. The “immediate” payments of PDI that Argentina is promising here don’t look like they come across as an attempt to “make current those debt obligations on the original bonds“, as the Second Circuit ordered.

We still can’t rule out a cramdown solution from the court for the pari passu saga. But if nothing else, Argentina’s proposal seems to show just how difficult doing this would be.

In the next part: GDP warrants, a strange argument over the price holdouts pay for their bonds, and Argentina ducks the question of its ability to pay any of this stuff.

Keine Kommentare:

Kommentar veröffentlichen