Clarin

Reserves fall another US$180 million

Thursday, October 31, 2013

The Central Bank reported last night that the fall in the reserves is not slowing down. It computed US$33.534 billion, US$180 million less than on Monday. The reasons for the drop obey the increasing exit of dollars needed for fuel imports and from spending by Argentine tourists abroad.

Precisely, as the importation of oil and its derivatives cannot be halted, what everyone in the market is waiting for is the announcement of new restrictions on the use of dollars by the general public. And eyes are pointed at the AFIP. It is expected that before the end of the year, a new ta will be implemented on credit card consumption, which would accentuate the “tourist dollar” market, arising from adding the AFIP tax, which is 20% today, to the official dollar rate.

The proximity of summer vacations indicates that the official decision shouldn’t take long to appear. That is, if there is not a turn to a more general measure, like a straight and full split currency exchange rate system.

The fall in reserves is deeper, but broken up because in September some US$1.5 billion entered in the form of a short-term loan. It was given by a European Central Bank that the BCRA doesn’t want to name over issues of confidentiality. In truth, it’s a loan guaranteed by the Central Bank reserves themselves, deposited in the Bank of Basel. They are there to be safe from attachments. But equally, there is not a plan in view to halt the fall of this asset.

La Nacion

By a nose, the IADB gave the country a credit

Thursday, October 31, 2013

by Martín Kanenguiser | LA NACION

The Inter-American Development Bank (IADB) approved yesterday, by a very narrow voting margin, a new US$300 million credit for Argentina.

The vote, once again, was very close due to the decision by most of the European countries and the United States to not support the granting of new loans to the country, a source close to the process in Washington told LA NACION.

"Nothing changed,” said the source bluntly with regard to Argentina’s yearning for the United States and other governments to start supporting the country since the announcement of the agreement with a group of companies in order to pay their sentences in the ICSID, the World Bank arbitration tribunal.

Sources from Washington indicated to LA NACION that they are waiting for the country to move forward in paying its debts to analyze a change in position, both in the IADB as well as the World Bank.

"There will be no changes until the government complies with all its obligations, both from the ICSID as well as the Paris Club,” they said.

In this direction, the government announced that it had already closed a deal with five companies that had won arbitration cases in the ICSID and UNCITRAL (the United Nations tribunal). They are National Grid, Continental, Vivendi, Azurix and CMS Gas.

Resolution 598 of the Economy Ministry, published on the 18th of this month in the Official Bulletin, established the payment of US$501 million to these five foreign companies.

The credit approved yesterday by the multinational entity led by Luis Alberto Moreno will serve for the “increasing, the rehabilitation and improvement of roadways, which include actions for improving the conditions of road safety in the region of Norte Grande of Argentina,” it detailed.

This IADB credit is part of a US$1.2 billion plan for Argentina this year, according to the plans of the regional bank, in which the United States has 30% of the shares.

For its part, Latin America has 53%, while Europe, China and Japan split the rest. If the outlook doesn’t change in the coming month, it will be difficult to see the World Bank approving some US$3 billion this year as announced by the government.

La Nacion

Economists do not predict changes in economic policy until 2015

They say that the political cost of some measures is too high, by which they expect the government will tighten the currency clamp and the draining of the reserves will continue

Thursday, October 31, 2013

by Florencia Donovan | LA NACION

Inflation and the exchange rate gap are only two of the macroeconomic variables that suggest that the model, as it was proposed 10 years ago, has run its course. However, and even despite Sunday’s election results, economists don’t believe that the government will make changes in economic policy in the next two years; on the contrary, the majority believes that it will seek to control the imbalances by deepening the recipes applied until now.

"After 10 years, a government has already given the best of itself. It’s naïve to think that it can make important changes,” said Guillermo Nielsen, Finance secretary during the presidency of Nestor Kirchner and, in that post, negotiator of the first debt swap of 2005.

"Look at what happened with the deepening of the currency exchange and the ridiculousness of the amnesty. I don’t think that there can be big changes. The issue these two years (until 2015) is what will happen with the heirs: is there anyone who wants to receive a macro-economy full of time bombs?” asked Nielsen, during a meeting organized by the magazine Bank at the Bolsa de Comercio.

The problem, according to Nielsen, is that many of the measures that seem obvious from the macroeconomic view, like the lag in prices relative to some sectors strongly affected by inflation, don’t seem possible from the political point of view. With inflation that, he said, is at around 30% annual, it’s difficult for example to think of adjustments in power rates of 100%, as are necessary in some cases.

Another of the big imbalances that is hitting the government at this time is the drop in reserves in the hands of the Central Bank. According to Martin Redrado, former BCRA president and current advisor to Sergio Massa, at the start of the year the majority of economists predicted that the reserves would remain stable in 2013, but they will end the year with a drop of US$11 billion. “The Central Bank cannot put up with a loss of US$1 billion per month,” said Redrado, for whom, however, in this “unending search for dollars” the government “will continue with more of the same.” “The government will now not be able to use reserves for sustaining growth and will have to protect them. This is equal to more clamp, more squeeze so that pre-financing for exports come,” he said.

Federico Sturzenegger, President of Banco Cuidad and now deputy-elect for the PRO, agreed: “Not much will change. The most likely is that we will see a stronger clamp, if there is not an interesting investment climate.”

But Sturzenegger said he is not concerned over the drainage of the reserves. For the economist, the problem is not the quality of reserves that a central bank has, but if it is credible or not. In Argentina, he said, the reserves are 8% of GDP, while in the United States they represent 1%. “Its credibility emanates from the other side,” said Sturzenegger. "In 2015, whatever the level of reserves, they will go up. Now, if a government without credibility like the current one releases the clamp it’s another slogan,” he said.

Only the BCRA former president and current director of Banco Hipotecario, Mario Blejer, ventured to say that the government is giving signals of having taken note of the need for a change. “To resume relations with the IMF and the Paris Club… I believe that there will be movements in that direction to untie the situation of the international market. In that sense, the problem of the reserves doesn’t worry by too much,” he said.

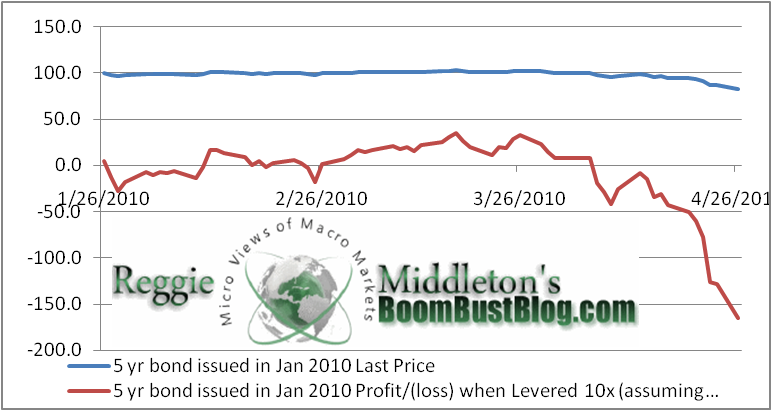

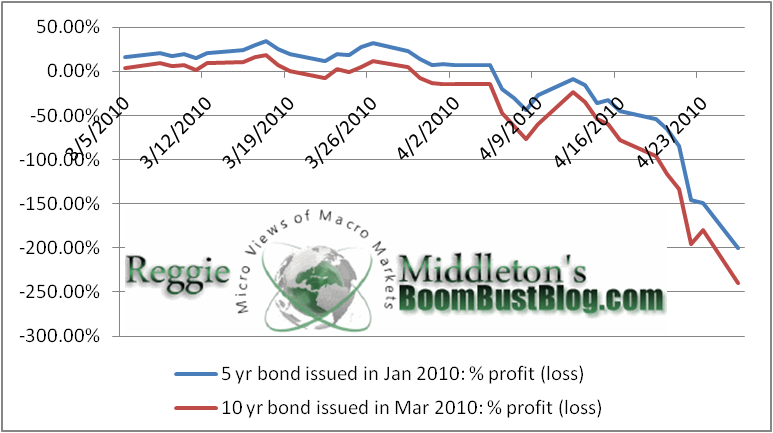

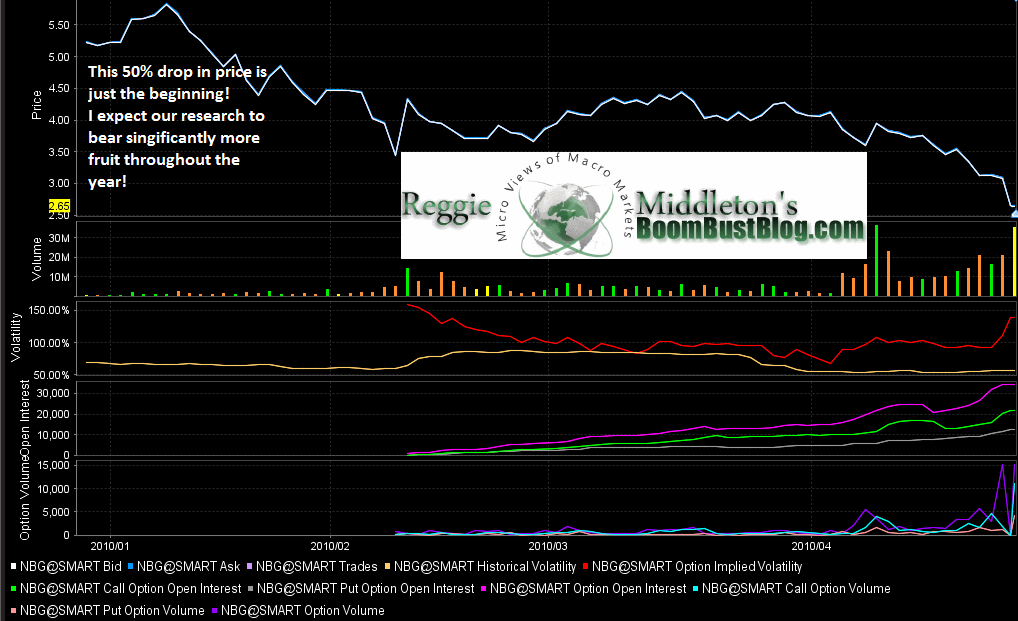

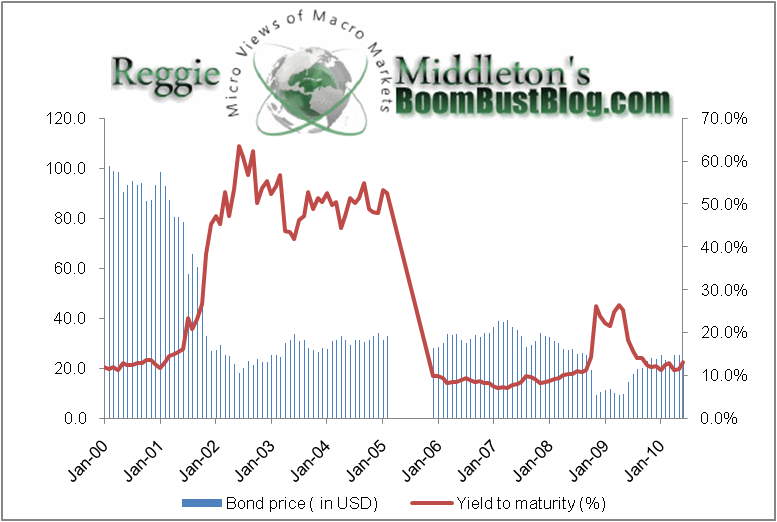

was the absolutely last thing the Greek banks needed as they were suffering from a classic run on the bank due to deposits being pulled out at a record pace. So assuming the aforementioned drain on liquidity from a bank run (mitigated in part or in full by support from the ECB), imagine what happens when a very significant portion of your bond portfolio performs as follows (please note that these numbers were drawn before the bond market route of the 27th)…

Und die Reisekosten müsste Mutti Sylvia dir doch eh wieder aus ihrem Strickgeld bezahlen.