Comparison of Greek and Argentinian Bond Restructuring Analysis

BOOKMARK / READ LATER

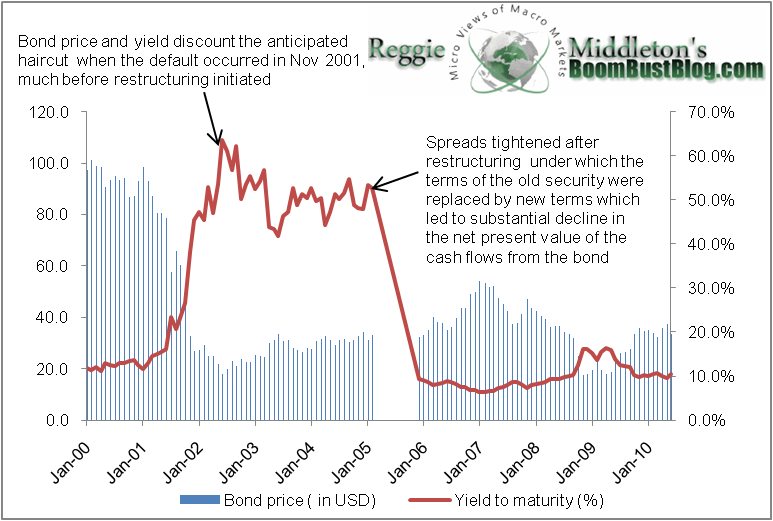

In order to assess the impact of sovereign debt restructuring on the market prices of the sovereign bonds that undergo restructuring (haircut in the principal amount or maturity extension), we retrieved price data of the Argentinean bonds that underwent restructuring in 2005. The sovereign debt restructuring in the case of Argentina was a combination of maturity extension and principal haircut. Argentina defaulted on its international debt in November 2001 after a failed attempt to restructure the debt. The markets priced in the risk of a substantial haircut around this time and the bond prices plummeted sharply. We at BoomBustBlog are in the habit of taking market prices seriously, and have factored historical market reactions into our analysis in calculating prospective price action in distressed and soon to be Sovereign debt. Before moving on, it is highly recommended that readers review our haircut analysis for Greece (“With the Euro Disintegrating, You Can Calculate Your Haircuts Here”) and our more likely to occur restructuring analysis for the same (What is the Most Likely Scenario in the Greek Debt Fiasco? Restructuring Via Extension of Maturity Dates).

restructuring on the market prices of the sovereign bonds that undergo restructuring (haircut in the principal amount or maturity extension), we retrieved price data of the Argentinean bonds that underwent restructuring in 2005. The sovereign debt restructuring in the case of Argentina was a combination of maturity extension and principal haircut. Argentina defaulted on its international debt in November 2001 after a failed attempt to restructure the debt. The markets priced in the risk of a substantial haircut around this time and the bond prices plummeted sharply. We at BoomBustBlog are in the habit of taking market prices seriously, and have factored historical market reactions into our analysis in calculating prospective price action in distressed and soon to be Sovereign debt. Before moving on, it is highly recommended that readers review our haircut analysis for Greece (“With the Euro Disintegrating, You Can Calculate Your Haircuts Here”) and our more likely to occur restructuring analysis for the same (What is the Most Likely Scenario in the Greek Debt Fiasco? Restructuring Via Extension of Maturity Dates).

restructuring on the market prices of the sovereign bonds that undergo restructuring (haircut in the principal amount or maturity extension), we retrieved price data of the Argentinean bonds that underwent restructuring in 2005. The sovereign debt restructuring in the case of Argentina was a combination of maturity extension and principal haircut. Argentina defaulted on its international debt in November 2001 after a failed attempt to restructure the debt. The markets priced in the risk of a substantial haircut around this time and the bond prices plummeted sharply. We at BoomBustBlog are in the habit of taking market prices seriously, and have factored historical market reactions into our analysis in calculating prospective price action in distressed and soon to be Sovereign debt. Before moving on, it is highly recommended that readers review our haircut analysis for Greece (“With the Euro Disintegrating, You Can Calculate Your Haircuts Here”) and our more likely to occur restructuring analysis for the same (What is the Most Likely Scenario in the Greek Debt Fiasco? Restructuring Via Extension of Maturity Dates).

The restructuring of the Argentina debt in default was occurred in 2005 when the government offered new bonds in exchange of old securities. The government gave the option of either accepting A) a par bond with no haircut in the principal amount but substantially lower coupon and longer maturity or accept B) a discount bond with a haircut in principal amount to the extent of 66.3% but relatively better coupon rate and shorter maturity than in case of Par bond. If the bondholder accepted A), for each unit of bond, one unit of Par bond will be allotted. If the bondholder accepted B), for each unit of bond, 0.33 unit of Discount Bond will be allotted. The loss to the creditor, which is decline in the NPV of the cash flows, was nearly the same in both cases as the lower principal amount in Option B was offset by better coupon rate and shorter maturity. The price of the par bond in the market and the price of the discount bond multiplied by the exchange ratio (real price to the bond holder) were largely the same when they were listed in the market in 2005.

in default was occurred in 2005 when the government offered new bonds in exchange of old securities. The government gave the option of either accepting A) a par bond with no haircut in the principal amount but substantially lower coupon and longer maturity or accept B) a discount bond with a haircut in principal amount to the extent of 66.3% but relatively better coupon rate and shorter maturity than in case of Par bond. If the bondholder accepted A), for each unit of bond, one unit of Par bond will be allotted. If the bondholder accepted B), for each unit of bond, 0.33 unit of Discount Bond will be allotted. The loss to the creditor, which is decline in the NPV of the cash flows, was nearly the same in both cases as the lower principal amount in Option B was offset by better coupon rate and shorter maturity. The price of the par bond in the market and the price of the discount bond multiplied by the exchange ratio (real price to the bond holder) were largely the same when they were listed in the market in 2005.

The IMF estimated the average haircut (decline in the net present value of the bond) was on an average 75% and the market priced in most of this haircut before the actual restructuring in Feb 2005. The prices of the bond in default declined nearly 65% between Feb 2001 and Feb 2005.

One should keep these figures in mind, for in the blog post “How Greece Killed Its Own Banks!“I ran through a much, much more optimistic scenario that wiped out ALL of the equity of the big Greek banks. Remember, the Greek government stuffed these banks to the gills with Greek bonds in order to created the perception of a market for them. As excerpeted…

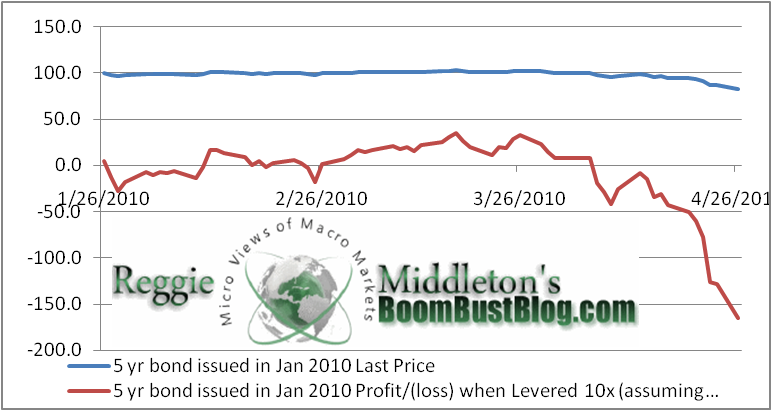

Well, the answer is…. Insolvency! The gorging on quickly to be devalued debt

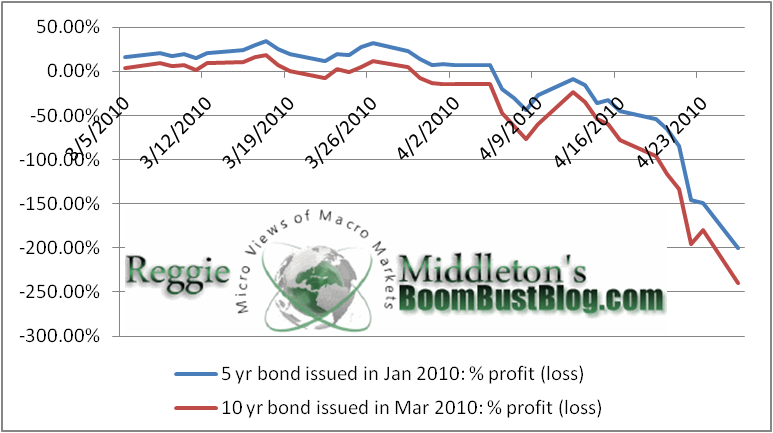

The same hypothetical leveraged positions expressed as a percentage gain or loss…

When I first started writing this post this morning, the only other bond markets getting hit were Portugal’s. After the aforementioned downgraded, I would assume we can expect significantly more activity. As you can, those holding these bonds on a leveraged basis (basically any bank that holds the bonds) has gotten literally toasted. We have discovered several entities that are flushed with sovereign debt and I am turning significantly more bearish against them. Subscribers, please reference the following:

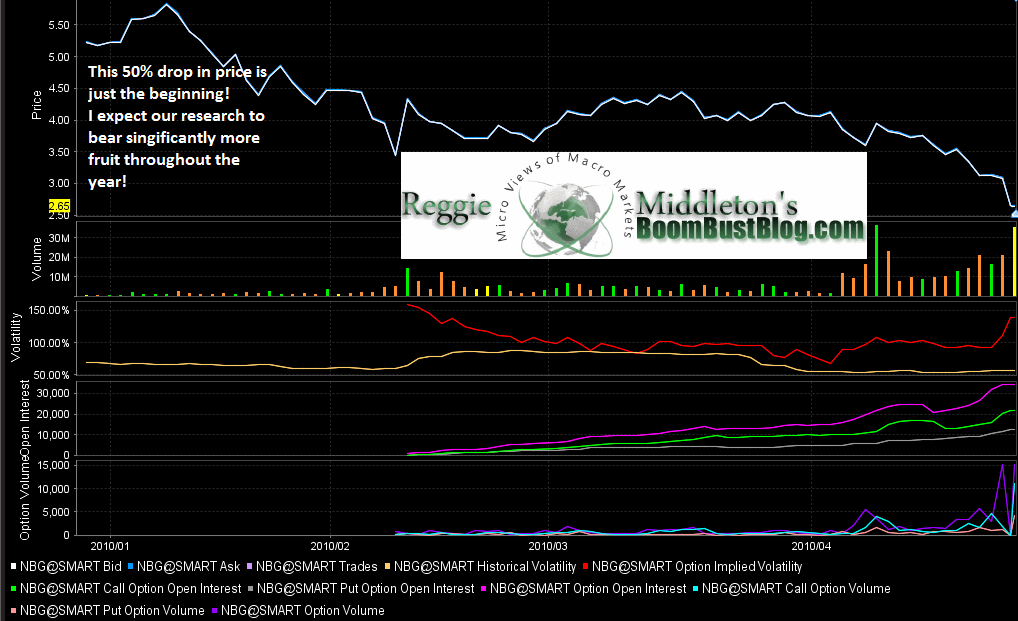

To date, my work both free and particularly the subscription work, has shown significant returns. I am quite confident that the thesis behind the Pan-European Sovereign Debt Crisis research is still quite valid and has a very long run ahead of it. Let’s look at one of the main Greek bank shorts that we went bearish on in January:

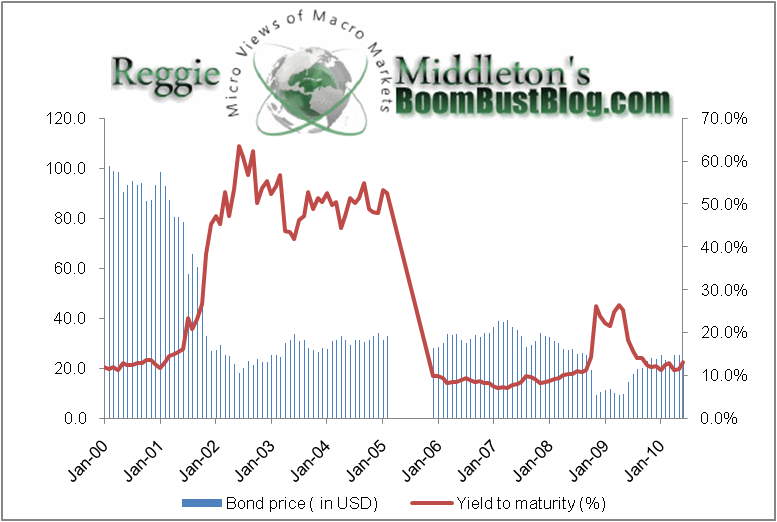

Now, referencing the bond price charts below as well as the spreadsheet data containing sovereign debt restructuring in Argentina, we get…

The price of the bond that went under restructuring and was exchanged for the Par bond in 2005.

Price of the bond that went under restructuring and was exchanged for the Discount bond

With this quick historical primer still fresh in our heads, let’s revisit ourGreek, Spanish, and Italian banking analyses (the green sidebar to the right), many of which are trying to push the 400% mark in terms of returns if one purchased OTM options at the time of the research release. It may be worthwhile to review the Sovereign debt exposure of Insurers and Reinsurers as well.

We may very well get a bear market rally or two that may pop prices, but from a fundamental perspective, I do not see how significantly more pain is not to come out of this debt fiasco. The only question is who’s next. We feel we have answered that question is sufficient detail through ourSovereign Contagion Model. Thus far, it has been right on the money for 5 months straight!

fiasco. The only question is who’s next. We feel we have answered that question is sufficient detail through ourSovereign Contagion Model. Thus far, it has been right on the money for 5 months straight!

Disclosure: Short greek banks

Keine Kommentare:

Kommentar veröffentlichen