Look ma, no uniquely recalcitrant sovereign

Part of the PARI PASSU SAGA SERIES

PASSU SAGA SERIES

Or not exciting. The saga might just get two years of a lame-duck president waiting to pass the holdout problem onto the next occupant of the Casa Rosada. (The Second Circuit also denied requests to lift the stay on the order for Argentina to pay holdouts on Friday, so we know the litigation is going to go on a bit longer.)

But that makes it all the more interesting to reconsider those recent, rather odd, whispers of a plan for Argentina’s restructured bondholders to go around the sovereign that really, really doesn’t want to pay — and make a deal for Elliott and co to go away themselves, dropping the demand of ratable payment from the Republic.

Remember of course that ratable payment might well logically imply inter-creditorlitigation, bondholders of one sovereign being free to sue each other to their piece of the pie. If Ruritania promised to pay Tom, Dick and Harry on the same basis, but (oops) left Harry out one day, an “injunction would run in the first instance against the borrower, but I believe… to Tom and Dick as well.” As it was once famously put.

So maybe inter-creditor negotiation is the only way to end an unstoppable order of ratable payment on an immovable debtor. And that might be a brave new world for sovereign debt.

The holdout tax

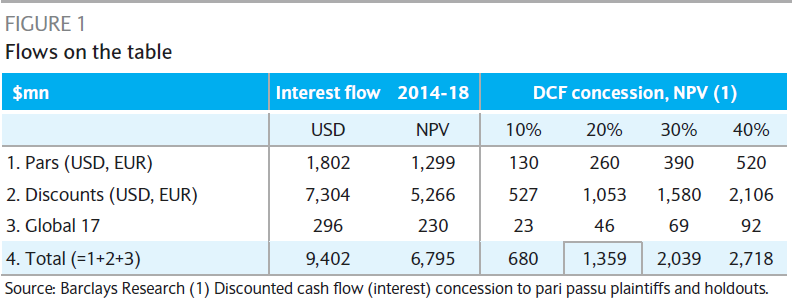

The actual details of the proposal — see the FT’s take on it last week, or the Argentine press a bit earlier — would have restructured holders turf over about 20 per cent of their coupon payments to holdouts, for about half a decade.

You could call this a “discounted cash flow concession”, as Barclays analysts Sebastian Vargas and Donato Guarino do in the chart below.

It sounds nicer than ‘holdout tax’.

The $1.3bn dollars or so of cash involved (on some strong assumptions of participation and so on) would go on top of what holdouts could get from signing up their bonds to Argentina’s usual restructuring offer. Argentina recently reopened it. Technically the plan doesn’t need Argentine involvement, but it does assume that offer remains available, and Argentina probably needs to sign a release anyway.

The restructured bondholders, for their pains, would at the very least safely get their remaining 80 per cent without it getting injuncted. But this isn’t the main point — that would be to unleash an enormous rally in Argentine bond prices that would overshadow the loss of the coupons, thanks to the government being able to borrow in the US again and generally not have Judge Griesa in its face.

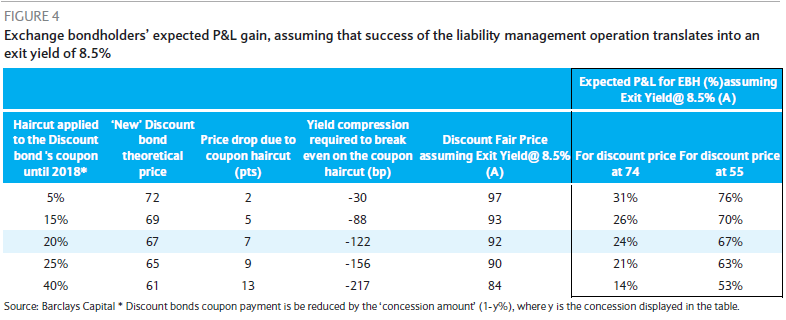

Higher prices overall after the deal might make more holdouts sign up. Exit yields would fall. That’s another chart on this from Barclays above. Note their assumption ofall holdouts signing up: every last Argentine abuela stiffed by her government back in 2001 (they’re not all foreign vulture funds). Although lower prices beforehand might be needed to get enough restructured holders to agree to send over bits of theircoupons. More on this in a bit.

The quality of Gramercy

But oh, oops — first, this is not a plan by restructured bondholders in the plural, just to be clear.

This is Gramercy’s plan. Gramercy Funds Management (“We are Emerging Markets®”) is one of the big players currently litigating tooth and nail against the ratable payment order, as part of the Exchange Bondholders Group.

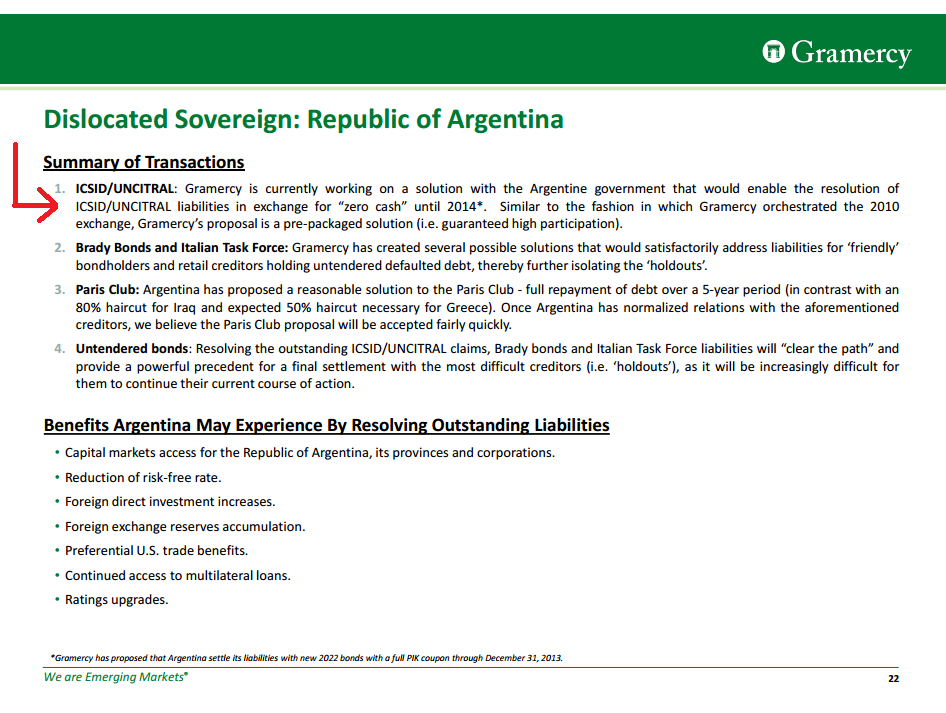

But they also have a very interesting sideline in cutting deals that help out the Argentine government (click to enlarge):

That’s a Gramercy Distressed Opportunity Fund II presentation from September 2012 — predicting, with astonishing clairvoyance, that a solution could be found to Argentina’s contretemps with holders of ICSID awards it also wouldn’t pay.

By October 2013, a solution was found: Argentina paid holders in US dollar local-law bonds (“zero cash…”) settling the claims and getting access to World Bank loans. It is not clear if Gramercy’s “pre-packaged solution… guaranteed high participation” from September 2012 involved buying up some of the ICSID claims itself at a discount — as reported.

There’s much more on Gramercy’s role in this recent Les Echos profile by Isabelle Couet. But needless to say — there’s some complexity here in the origins of this inter-creditor deal.

Not least, other exchange bondholders have other ideas about how to negotiate. One is to wait until Argentina has defaulted on everyone, if or when the US courts have finally gone against it… take the pain which default would cause to restructured bond prices, and only then go talk to the pari passu plaintiffs. In theory, they couldn’t use default as leverage on their side by that point. It’s a bit like Thomas Schelling androcking the boat.

Still, with all that in mind — is the plan actually realistic? We have three points.

1.) The plan needs 85 per cent of exchange bondholders to sign up to it overall. That’s the threshold for activating the aggregate collective action clause contained in the restructured debt’s terms, the one needed to alter “all affected” bonds rather than just one series. Which is why Gramercy has been busy shopping the plan around other investors.

In terms of principle, there might be restructured investors who just refuse to give up their coupons. They’ve restructured once, for a start. But there are particular bonds (say, under English rather than New York) whose holders have consistently argued that the original injunction on Argentina shouldn’t at all apply to payments owed to them. So why cut their coupons now?

In terms of price, though, it might get tricky. There’s already been a fairly big rally in Argentine bonds, because of the ICSID settlement, but also because Kirchnerism seems to be going out of style with a vengeance.

So, there might be quite a few investors who sold into this rally at much higher prices than a month or two ago. The new owners of the bonds, bought as much as 20 points dearer in price, may not like so much the idea of a coupon cut.

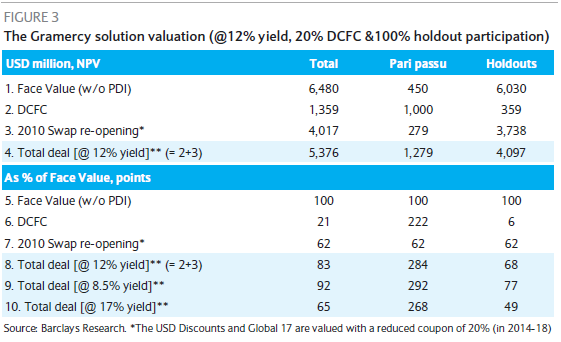

Still, money, or capital appreciation, might talk. A third chart from Barclays:

2.) But the plan also needs the highest level of participation from the other side. Holdouts, including pari passu plaintiffs. You could say that’s simple to get — only about three or four funds are currently driving the pari passu litigation. So once they’re won over to a suitably remunerative proposal, a deal should be sewn up. And you could well be wrong.

If you go back to the logic of ratable payment, Harry might be able to sue Tom and Dick, and potentially Tom and Dick can settle with Harry. But maybe Sue can sue Harry too, if Sue has received nothing from the borrower. She could also crank out injunctions against her uniquely recalcitrant borrower whenever it tried to borrow in the US, in the meantime — note the ‘normalisation’ case for Argentina’s benefit from an inter-creditor deal… — but it’s worth contemplating the prospect of some holdouts remaining… holdouts, and suing holdouts who took whatever comes out of Gramercy’s proposal.

That might not be realistic. Not every Argentine holdout can afford Elliott’s legal fees. Still, as Barclays point out, the current proposal implies that the amount of subsidy to each holdout falls the more pari passu plaintiffs who sign up, leaving the remaining holdouts in an interesting position — which is why they’ve run the numbers with a “conservative assumption” of 100 per cent participation.

3.) If the plan goes ahead and it doesn’t work, the sovereign bond market might still get left with it as a precedent. Intercreditor agreements aren’t unusual in corporate debt restructuring. There, you might find some (therefore junior) creditors agreeing to turn over payments they get to other (therefore senior) creditors, if the borrower hasn’t paid the latter fully. But that presupposes the concepts of senior and junior creditors… collateral… and corporate bankruptcy, as the alternative place to fight this stuff out.

Sovereigns don’t go bankrupt. More to the point they’re not supposed to have hierarchies of creditor either… openly. At least not among bondholders. Restructured holders agreeing to remit parts of their coupons might be taken as recognition on their part that you get a special status if you’re a holdout and you can hang around long enough.

So why announce the plan?

Possibly because it just undercuts the pari passu holdouts’ leverage a bit at the moment — they’re still winning in the courts (notwithstanding the stay remaining in place), and have the confidence to tell Argentina itself to come to the table.

But even then the pari passu saga — and with it the frontier of sovereign debt litigation — is getting ever more involved in inter-creditor negotiation…

Ads not by this site

The "trial of the century" in sovereign debt restructuring, in our humble opinion. The story of Argentina, its holdout creditors, the grande finale (or is it?) of their battle in US courts.

Keine Kommentare:

Kommentar veröffentlichen